Reverse Charge VAT For CIS Construction Services

If you are CIS registered and VAT registered, then from the 1st of March 2021 there will be changes to the way you account for VAT. This blog investigates these changes and what they mean for your business.

The changes mean a VATregistered business, which supplies certain construction services to another VAT-registered business for onward sale, will be required to issue a VAT invoice stating that the service is subject to the domestic reverse charge.

And the recipient of the invoice must account for the VAT due on that supply through its VAT return, instead of paying the VAT amount to the supplier. The recipient may recover that VAT amount as input Tax, subject to the normal rules.

So, what does this mean in practice?

A – Roofing Company Limited (who is VAT registered) supplies the materials and roofs for a new office building (£100,000 + VAT) to B – Developer Limited (who is also VAT registered). B Developer Limited will sell the finished commercial building to C – The end-user, its client.

A – Roofing Company Limited would, under the old system, invoice B – Developer Limited

£120,000, comprising of his £100,000 plus £20,000 in VAT (at 20%).

• Under the new CIS reverse charge mechanism, A – Roofing Company would still invoice the £100,000 but state that the CIS reverse charge applies on the invoice and that the applicable rate of VAT is 20%.

• B – Developer Limited pays A Roofing Company Limited the net £100,000 fee. It then accounts for output and input VAT of £20,000 on the supply on its own VAT return.

• Because of the reverse charge procedure, A – Roofing Company Limited receives £20,000 less cash. However, they do not have to account to HMRC for any output tax on the transaction and therefore won’t pay over the £20,000 to HMRC.

• When A – Roofing Company Limited is paid, they include the value of the sale in box 6 of the VAT Return. They do not add it to box 1 as they receive no VAT.

Effects on Cashflow

• The change may well have a negative impact on A – Roofing Company Limited’s cashflow, as under the old rules, if B – Developer Limited was a prompt payer, A – Roofing Company Limited could hope that they could use the £20,000 in VAT to purchase his materials. They could then purchase materials and offset the input tax paid against the output liability before they have to pay over the Net VAT to HMRC.

• B – Developer Limited has a cashflow advantage as they do not have to pay the £20,000 VAT and this also means at the end of its VAT quarter it cannot reclaim £20,000 as it is accounting for the reverse charge and the output VAT offsets the input VAT.

• As B – Developer Limited is supplying CIS services, it must be satisfied that its client is the end-user and is not going to be involved in the onward supply of CIS services. In this case, C -The end-user, is an investor and has issued B with and end-user statement so that the reverse charge does not apply.

The conditions for the CIS reverse charge to be applied are:

• The supply for VAT consists of construction services and materials.

• Made at the standard or reduced rate of VAT.

• Between a UK VAT, registered supplier and UK VAT registered customer.

• Supplier and customer are registered for CIS.

• The customer intends to make an ongoing supply of construction services to another party.

• The supplier and customer are not connected.

The CIS reverse charge does not apply to any of the following supplies:

• Supplies of VAT exempt building and construction services.

• Supplies that are not covered by the CIS, unless linked to such a supply.

• Supplies of staff or workers.

The CIS reverse charge does not apply to taxable supplies made to the following customers:

• A non-VAT registered customer

• ‘End Users,’ i.e. a VAT registered customer who is not intending to make further ongoing supplies of construction. In these circumstances, the default position is that the reverse charge for VAT applies unless confirmation of end-user statement is issued.

• Intermediary customers who are connected, e.g. a landlord and his tenant, two companies in the same group.

The aim of the measure is to reduce VAT fraud in the construction sector.

It will require a significant change of approach in many CIS businesses:

• Staff will need to be trained to identify relevant CIS contracts and End Users.

• Accounting and bookkeeping systems will need to be modified to cope with the new invoicing and reporting obligations.

• The use of the VAT Flat Rate Scheme and Cash accounting may not be possible.

• Cashflow will be affected, and those at the start of the supply chain may become VAT repayment claimants: they need to consider whether to file monthly returns.

• It may require a business who is the recipient of the supply to VAT register.

If you think that you will be affected by this change then get in touch, we will be happy to help.

VAT: domestic reverse charge for building and construction services

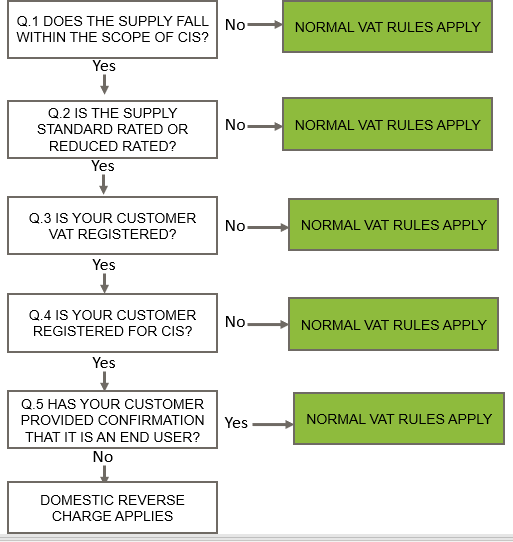

Annex 1 Use this flowchart to see how you would decide whether to apply normal VAT rules,or apply the domestic reverse charge. Do not use it for services supplied by employment businesses.